Breaking Bank Boundaries — SoFi Technologies, Inc. Becomes the First to Let Bank Clients Trade Crypto

Introduction: Banks and Crypto—A New Era

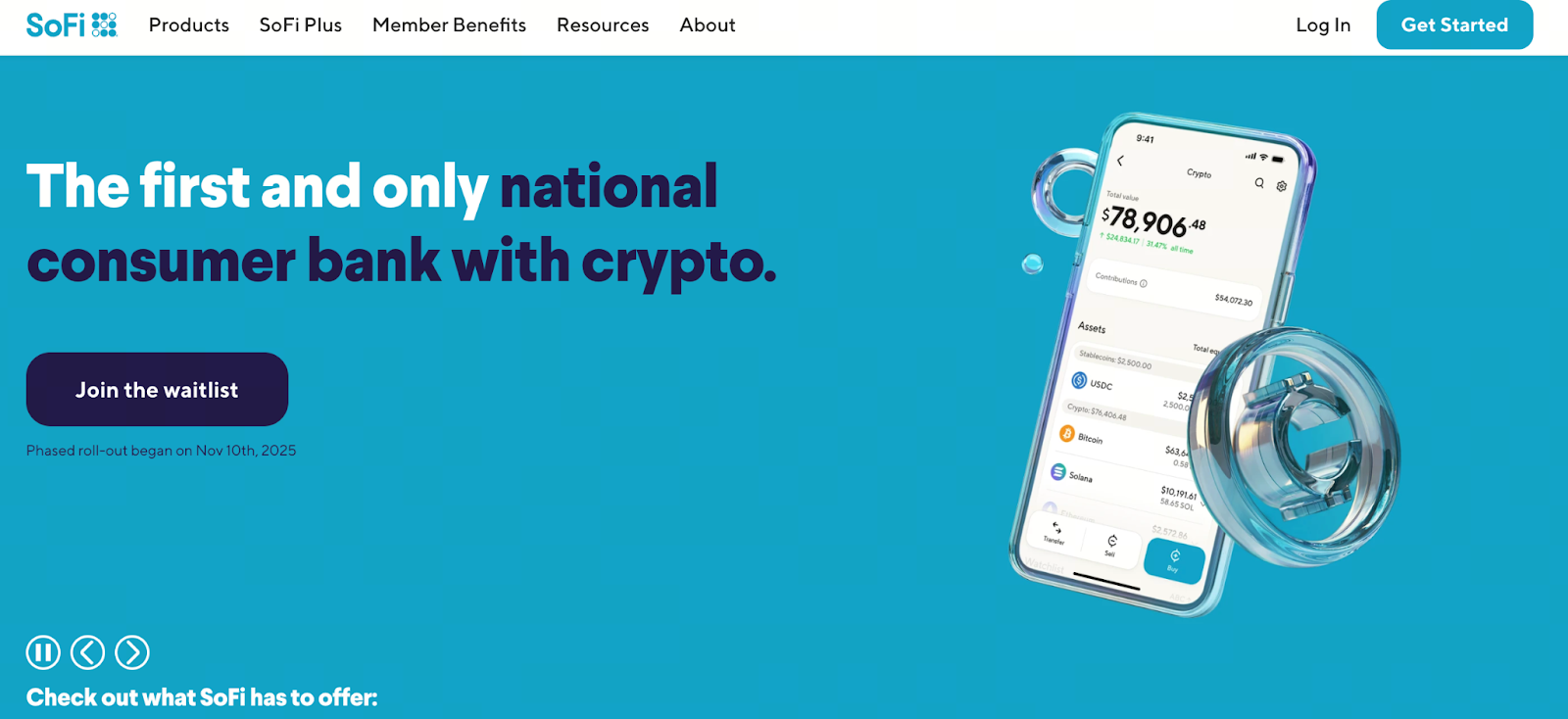

Image: https://www.sofi.com/

Traditional banking has largely centered on savings, lending, and wealth management, while cryptocurrency has emerged as a leading force in fintech innovation. SoFi is breaking new ground by merging banking services and crypto asset trading into a single platform. Users can buy and sell cryptocurrencies like BTC, SOL, and ETH directly from their bank accounts, eliminating the need for external exchanges. This innovation enables everyday users to purchase crypto within their banking platform. It marks a pivotal step toward bringing crypto assets into the financial mainstream.

Why Is SoFi Leading the Charge?

By 2025, SoFi’s membership surpassed 12.6 million users, giving it several key advantages. The company previously partnered with Coinbase in 2019 to offer crypto trading, but paused the service in 2023 to secure a banking license. Now, with a national banking license in hand, SoFi uniquely positions itself at the intersection of traditional banking and fintech. Meanwhile, recent regulatory shifts have clarified how banks can participate in crypto asset services. This strategic move positions SoFi at the forefront of the evolving crypto-banking model. This model may soon set a new industry standard.

Service Overview: One-Stop Banking and Crypto Asset Platform

The SoFi Crypto service introduces several key features:

- Users can buy, sell, and hold a variety of cryptocurrencies within the SoFi banking app (with initial support for BTC, ETH, SOL, and more).

- Funding is sourced directly from users’ bank accounts, eliminating the need for separate deposits, transfers, or cross-platform transactions. SoFi confirms that both checking and savings balances can be used for trading.

- The platform adheres to bank-level security and compliance standards, though crypto assets are not insured by the Federal Deposit Insurance Corporation (FDIC) or Securities Investor Protection Corporation (SIPC).

- The service is being rolled out in phases. It is initially available to select members, with expansion to all members expected in the coming weeks.

Market Context and Regulatory Evolution

What’s driving traditional banks to enter crypto asset trading now? Key factors include:

- Growing adoption: SoFi reports that approximately 60% of its crypto-holding members prefer managing digital assets through a licensed bank rather than a traditional exchange.

- Regulatory progress: U.S. regulators signaled in 2025 that banks may provide crypto asset services under compliant conditions.

- Industry momentum: SoFi’s launch may serve as a benchmark for other banks to follow suit.

Banking and crypto are converging at a rapidly accelerating pace.

Implications for Users: Balancing Opportunity and Risk

Opportunities:

- For the first time, traditional banking and crypto trading are unified, delivering a more user-friendly experience for non-experts by streamlining transfers, reducing fees, and simplifying platform navigation.

- Backed by a banking license, user confidence increases, especially among those previously deterred by security concerns at exchanges.

- Easy access to crypto through a familiar banking interface could attract new users and accelerate crypto adoption.

Risks:

- Crypto assets are not deposits and are not protected by FDIC or SIPC. SoFi explicitly warns that crypto assets could lose all their value.

- Exchange capabilities, liquidity, and supported assets are initially limited to a select group of major cryptocurrencies.

- Users trading directly from their bank accounts should remain vigilant—convenience does not mean less risk.

Users should carefully assess their risk tolerance, as crypto assets should be treated as high-risk investments.

Conclusion: The Bank-Crypto Era Has Arrived

SoFi’s initiative is more than just a merger of traditional banking and crypto—it may signal a reshaping of the financial ecosystem itself. As banks begin to offer savings, lending, investment, and crypto trading in one place, the boundaries of financial services are blurring. For individual users, this provides a convenient entry point, but it’s essential to remain mindful of the inherent risks. Those considering accessing crypto assets through their bank should first understand the platform’s rules, asset characteristics, and their personal risk profile.

Looking ahead, more banks are expected to roll out similar services, potentially accelerating mainstream acceptance of crypto assets.

Share

Content

Related Articles

Pi Coin Transaction Guide: How to Transfer to Gate.io

Flare Crypto Explained: What Is Flare Network and Why It Matters in 2025

How to Use a Crypto Whale Tracker: Top Tool Recommendation for 2025 to Follow Whale Moves

What is N2: An AI-Driven Layer 2 Solution

2025 BTC Price Prediction: BTC Trend Forecast Based on Technical and Macroeconomic Data