#USOCCIssuesNewStablecoinRules

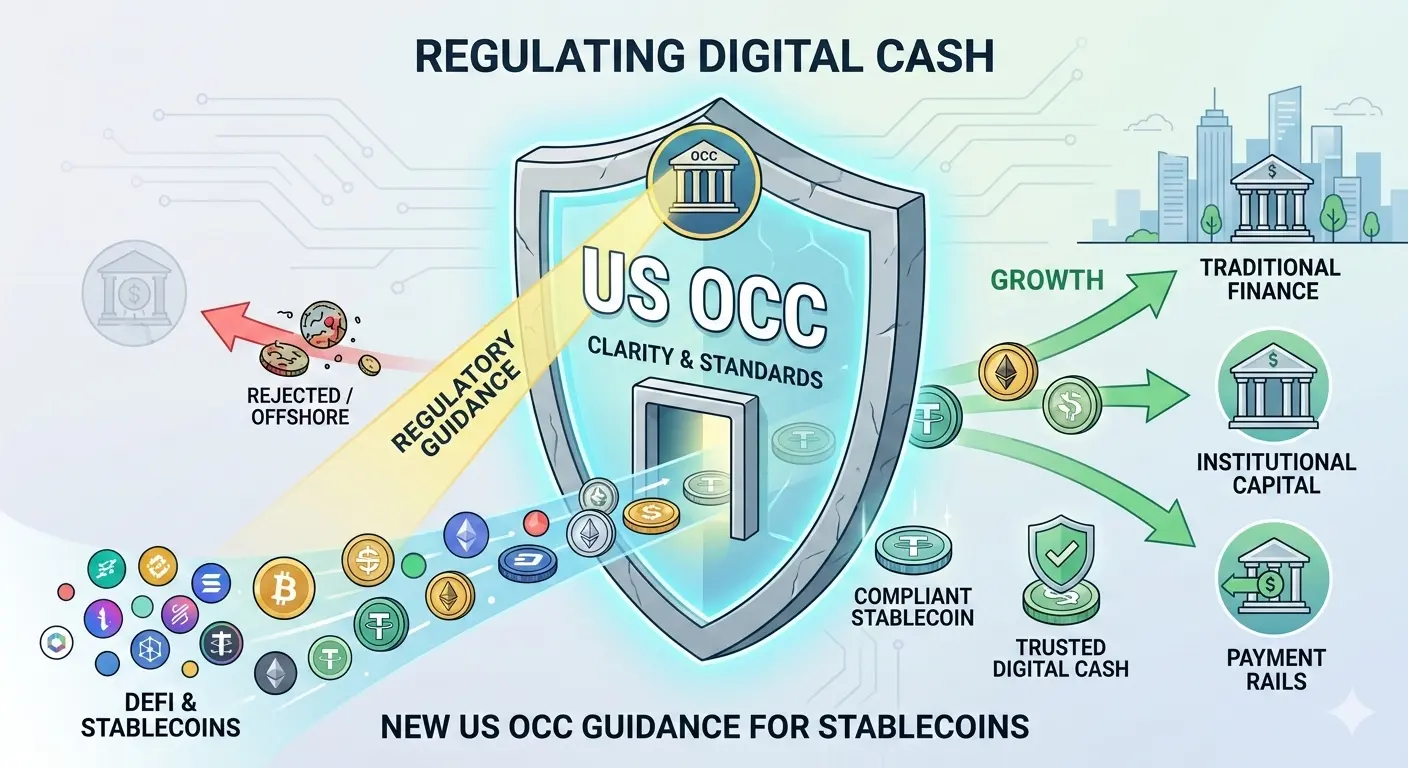

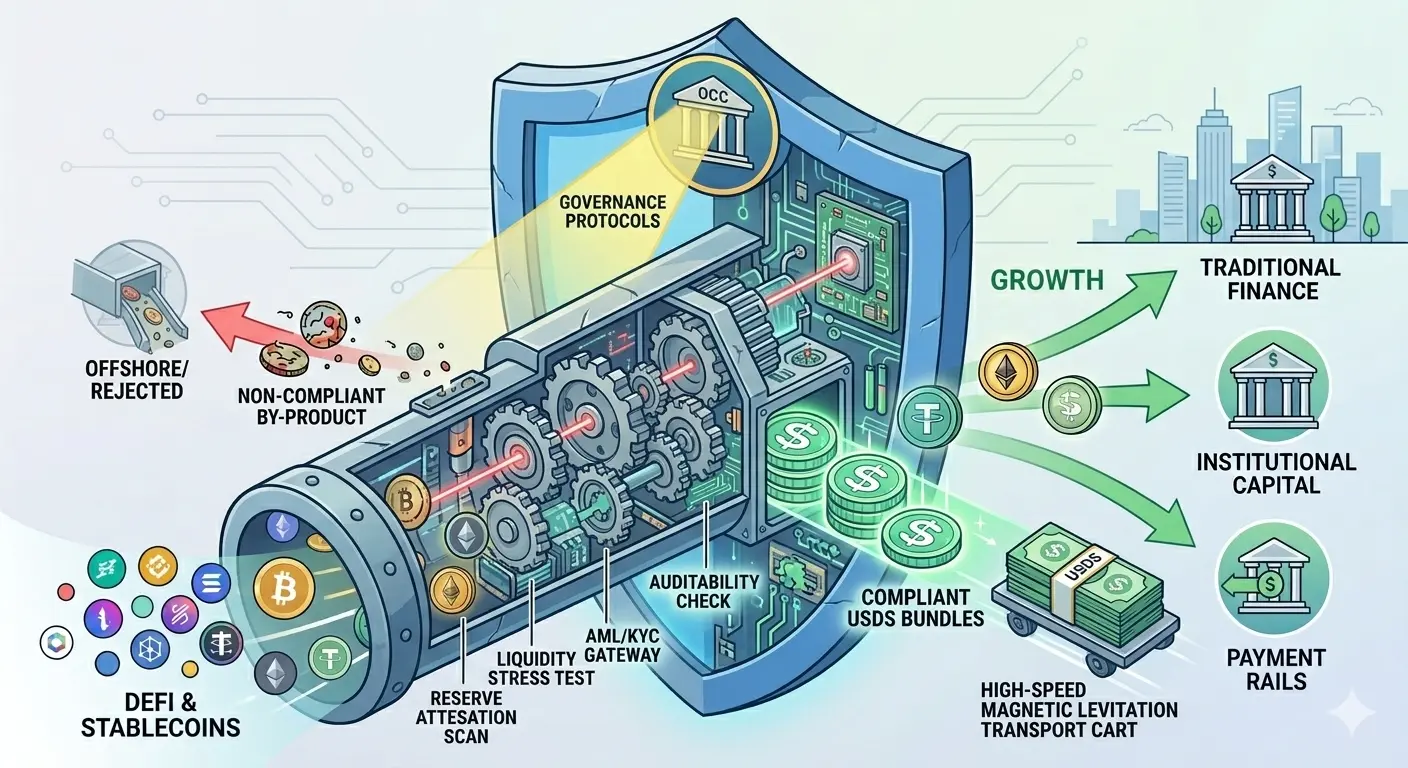

The U.S. Office of the Comptroller of the Currency (OCC) has taken a landmark step in crypto regulation by issuing a comprehensive Notice of Proposed Rulemaking (NPRM) on February 25, 2026, to implement key provisions of the Guiding and Establishing National Innovation for U.S. Stablecoins Act (commonly known as the GENIUS Act), which was signed into law on July 18, 2025. This 376-page proposal—often referred to in headlines as the "new stablecoin rules"—lays out the first detailed federal supervisory framework specifically for payment stablecoins (USD-pegged digital assets designed for payments and settlement). It applies to entities under OCC jurisdiction, including national bank subsidiaries, federal qualified issuers, certain state-qualified issuers, and foreign issuers operating in the U.S.

.

1. Background: The GENIUS Act and Why the OCC's Proposal Matters

GENIUS Act Overview (Enacted July 18, 2025): Establishes a federal framework for "payment stablecoins" — digital assets that maintain a stable value relative to fiat currency (primarily USD) and are intended for use as a means of payment or settlement.

Core prohibitions: Only "permitted payment stablecoin issuers" (PPSIs) can issue payment stablecoins in the U.S. Digital asset service providers (e.g., exchanges) generally cannot offer or sell them to U.S. persons unless issued by a PPSI or qualifying foreign issuer.

The Act left detailed rules (capital, liquidity, reserves, risk management, etc.) to federal regulators like the OCC to implement via rulemaking.

OCC's Role: As the primary regulator for national banks and certain nonbanks, the OCC now proposes new Part 15 to Title 12 of the Code of Federal Regulations. This covers issuance, custody, reserves, redemption, capital, and more for OCC-supervised entities.

Effective Date Timeline: The GENIUS Act becomes effective 18 months after enactment (January 2027) or 120 days after final rules from primary regulators—whichever comes first. The OCC's proposal is a major piece; comments are due 60 days after Federal Register publication (expected early March 2026).

2. Scope and Who It Applies To

Permitted Payment Stablecoin Issuers (PPSIs) under OCC jurisdiction:

Subsidiaries of national banks or federal savings associations.

Federal qualified nonbank issuers.

State-qualified nonbank issuers (if they exceed $10 billion in issuance, they must transition to federal oversight within 360 days or cease net new issuance; waiver possible).

Foreign payment stablecoin issuers (OCC has regulatory authority).

Excludes non-payment stablecoins (e.g., algorithmic or yield-bearing tokens) and issuers without OCC authority.

Also covers custody activities by OCC-supervised banks (e.g., holding reserves or stablecoins).

3. Key Requirements in the Proposed Rules

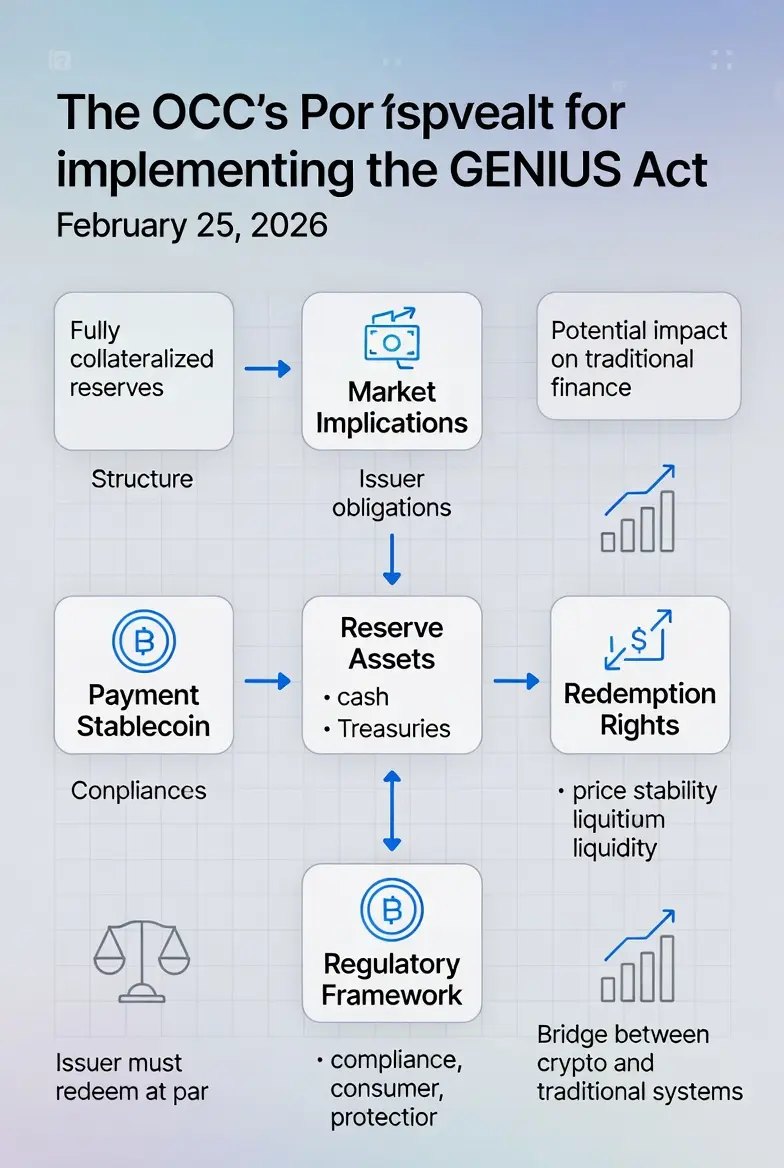

Reserve Assets (1:1 Backing):

Issuers must hold identifiable, segregated reserves with fair value ≥ outstanding stablecoins at all times.

Permissible assets: High-quality, liquid items (e.g., U.S. Treasuries, central bank deposits, cash equivalents—mirroring GENIUS Act list).

Reserves can be held directly or via eligible custodians (including affiliates).

Strict segregation and record-keeping to prevent commingling.

Redemption Rights:

Holders must be able to redeem stablecoins promptly at par value (1:1 with USD).

Clear processes for timely redemption, even in stress scenarios.

Capital Requirements:

Minimum $5 million for newly formed (de novo) issuers.

Risk-based capital for ongoing operations to ensure safety and soundness.

Prohibition on Interest/Yield:

Bright-line ban: PPSIs cannot pay interest, yield, or rewards to holders solely for holding/using/retaining the stablecoin.

Rebuttable presumption against arrangements where issuers pay yield to third parties (e.g., affiliates/exchanges) that then pass it to holders—aimed at preventing bypass via white-label or partnership models.

This could impact platforms like Coinbase (which shares revenue with issuers like Circle for USDC rewards).

Risk Management & Operational Standards:

Robust policies for liquidity, operational risk, cybersecurity, AML/BSA compliance (separate rulemaking pending).

Limits on activities to prevent balance-sheet expansion beyond core payment functions.

Licensing & Supervision:

Application process for becoming a PPSI.

Ongoing examination, reporting (quarterly), and enforcement authority.

Potential restriction: One brand per issuer (with streamlined affiliate approvals) to reduce contagion risks.

4. Why This Matters: Broader Context and Goals

Clarity & Safety: Ends years of uncertainty post-2022 collapses (e.g., TerraUSD, concerns over Tether/USDC reserves).

Integration with Traditional Finance: Encourages banks to issue or custody stablecoins safely, bridging TradFi and crypto.

Consumer Protection: 1:1 reserves, audits, and redemption reduce run risks and fraud.

Innovation Balance: Aims to let the industry "flourish in a safe and sound manner" while preventing misuse.

Global Impact: Sets a precedent; foreign issuers must comply if serving U.S. users.

5. Market Implications & Potential Effects

Positive for Regulated Issuers:

USDC (Circle) and similar bank-affiliated tokens could gain trust and institutional adoption.

Banks may enter/expand stablecoin activities confidently.

Challenges & Risks:

Yield/reward restrictions could pressure business models (e.g., DeFi integrations, exchange incentives).

Compliance costs may raise barriers for smaller issuers.

Short-term volatility if markets interpret rules as restrictive.

Stablecoin Market Reaction:

Major USD stablecoins (USDT, USDC, DAI, etc.) dominate ~$150B+ market cap.

Proposal reinforces USD dominance but could shift volume to fully compliant issuers.

Institutional inflows may accelerate; retail/DeFi users watch for yield impacts.

Broader Crypto Ecosystem:

Boosts legitimacy, potentially lifting ETH/BTC sentiment amid regulatory progress.

Complements other efforts (e.g., Clarity Act discussions).

If finalized, could reduce offshore risks and enhance U.S. competitiveness.

6. Next Steps & How to Engage

Comment Period: 60 days from Federal Register publication—industry groups, issuers, and users encouraged to submit feedback.

Final Rule: Expected later in 2026; could evolve based on comments.

Monitoring: Track OCC site, Federal Register, and updates from issuers like Circle/Paxos.

Conclusion

The OCC's February 25, 2026, proposal to implement the GENIUS Act marks the most comprehensive federal stablecoin framework yet—shifting from guidance/interpretive letters to enforceable rules. It prioritizes safety, transparency, and 1:1 backing while banning yield to keep stablecoins cash-like. This bridges traditional banking and digital assets, fostering responsible growth but requiring adaptation from issuers and platforms.

Short-term: Expect scrutiny on yield models and compliance adjustments. Long-term: Stronger foundation for mainstream adoption and institutional confidence.

The U.S. Office of the Comptroller of the Currency (OCC) has taken a landmark step in crypto regulation by issuing a comprehensive Notice of Proposed Rulemaking (NPRM) on February 25, 2026, to implement key provisions of the Guiding and Establishing National Innovation for U.S. Stablecoins Act (commonly known as the GENIUS Act), which was signed into law on July 18, 2025. This 376-page proposal—often referred to in headlines as the "new stablecoin rules"—lays out the first detailed federal supervisory framework specifically for payment stablecoins (USD-pegged digital assets designed for payments and settlement). It applies to entities under OCC jurisdiction, including national bank subsidiaries, federal qualified issuers, certain state-qualified issuers, and foreign issuers operating in the U.S.

.

1. Background: The GENIUS Act and Why the OCC's Proposal Matters

GENIUS Act Overview (Enacted July 18, 2025): Establishes a federal framework for "payment stablecoins" — digital assets that maintain a stable value relative to fiat currency (primarily USD) and are intended for use as a means of payment or settlement.

Core prohibitions: Only "permitted payment stablecoin issuers" (PPSIs) can issue payment stablecoins in the U.S. Digital asset service providers (e.g., exchanges) generally cannot offer or sell them to U.S. persons unless issued by a PPSI or qualifying foreign issuer.

The Act left detailed rules (capital, liquidity, reserves, risk management, etc.) to federal regulators like the OCC to implement via rulemaking.

OCC's Role: As the primary regulator for national banks and certain nonbanks, the OCC now proposes new Part 15 to Title 12 of the Code of Federal Regulations. This covers issuance, custody, reserves, redemption, capital, and more for OCC-supervised entities.

Effective Date Timeline: The GENIUS Act becomes effective 18 months after enactment (January 2027) or 120 days after final rules from primary regulators—whichever comes first. The OCC's proposal is a major piece; comments are due 60 days after Federal Register publication (expected early March 2026).

2. Scope and Who It Applies To

Permitted Payment Stablecoin Issuers (PPSIs) under OCC jurisdiction:

Subsidiaries of national banks or federal savings associations.

Federal qualified nonbank issuers.

State-qualified nonbank issuers (if they exceed $10 billion in issuance, they must transition to federal oversight within 360 days or cease net new issuance; waiver possible).

Foreign payment stablecoin issuers (OCC has regulatory authority).

Excludes non-payment stablecoins (e.g., algorithmic or yield-bearing tokens) and issuers without OCC authority.

Also covers custody activities by OCC-supervised banks (e.g., holding reserves or stablecoins).

3. Key Requirements in the Proposed Rules

Reserve Assets (1:1 Backing):

Issuers must hold identifiable, segregated reserves with fair value ≥ outstanding stablecoins at all times.

Permissible assets: High-quality, liquid items (e.g., U.S. Treasuries, central bank deposits, cash equivalents—mirroring GENIUS Act list).

Reserves can be held directly or via eligible custodians (including affiliates).

Strict segregation and record-keeping to prevent commingling.

Redemption Rights:

Holders must be able to redeem stablecoins promptly at par value (1:1 with USD).

Clear processes for timely redemption, even in stress scenarios.

Capital Requirements:

Minimum $5 million for newly formed (de novo) issuers.

Risk-based capital for ongoing operations to ensure safety and soundness.

Prohibition on Interest/Yield:

Bright-line ban: PPSIs cannot pay interest, yield, or rewards to holders solely for holding/using/retaining the stablecoin.

Rebuttable presumption against arrangements where issuers pay yield to third parties (e.g., affiliates/exchanges) that then pass it to holders—aimed at preventing bypass via white-label or partnership models.

This could impact platforms like Coinbase (which shares revenue with issuers like Circle for USDC rewards).

Risk Management & Operational Standards:

Robust policies for liquidity, operational risk, cybersecurity, AML/BSA compliance (separate rulemaking pending).

Limits on activities to prevent balance-sheet expansion beyond core payment functions.

Licensing & Supervision:

Application process for becoming a PPSI.

Ongoing examination, reporting (quarterly), and enforcement authority.

Potential restriction: One brand per issuer (with streamlined affiliate approvals) to reduce contagion risks.

4. Why This Matters: Broader Context and Goals

Clarity & Safety: Ends years of uncertainty post-2022 collapses (e.g., TerraUSD, concerns over Tether/USDC reserves).

Integration with Traditional Finance: Encourages banks to issue or custody stablecoins safely, bridging TradFi and crypto.

Consumer Protection: 1:1 reserves, audits, and redemption reduce run risks and fraud.

Innovation Balance: Aims to let the industry "flourish in a safe and sound manner" while preventing misuse.

Global Impact: Sets a precedent; foreign issuers must comply if serving U.S. users.

5. Market Implications & Potential Effects

Positive for Regulated Issuers:

USDC (Circle) and similar bank-affiliated tokens could gain trust and institutional adoption.

Banks may enter/expand stablecoin activities confidently.

Challenges & Risks:

Yield/reward restrictions could pressure business models (e.g., DeFi integrations, exchange incentives).

Compliance costs may raise barriers for smaller issuers.

Short-term volatility if markets interpret rules as restrictive.

Stablecoin Market Reaction:

Major USD stablecoins (USDT, USDC, DAI, etc.) dominate ~$150B+ market cap.

Proposal reinforces USD dominance but could shift volume to fully compliant issuers.

Institutional inflows may accelerate; retail/DeFi users watch for yield impacts.

Broader Crypto Ecosystem:

Boosts legitimacy, potentially lifting ETH/BTC sentiment amid regulatory progress.

Complements other efforts (e.g., Clarity Act discussions).

If finalized, could reduce offshore risks and enhance U.S. competitiveness.

6. Next Steps & How to Engage

Comment Period: 60 days from Federal Register publication—industry groups, issuers, and users encouraged to submit feedback.

Final Rule: Expected later in 2026; could evolve based on comments.

Monitoring: Track OCC site, Federal Register, and updates from issuers like Circle/Paxos.

Conclusion

The OCC's February 25, 2026, proposal to implement the GENIUS Act marks the most comprehensive federal stablecoin framework yet—shifting from guidance/interpretive letters to enforceable rules. It prioritizes safety, transparency, and 1:1 backing while banning yield to keep stablecoins cash-like. This bridges traditional banking and digital assets, fostering responsible growth but requiring adaptation from issuers and platforms.

Short-term: Expect scrutiny on yield models and compliance adjustments. Long-term: Stronger foundation for mainstream adoption and institutional confidence.